BATON ROUGE (Nov. 1, 2024) — In a bold move aimed at reshaping Louisiana’s fiscal landscape, Governor Jeff Landry has announced plans to convene a special legislative session from Tuesday through November 25, focusing on an overhaul of the state’s tax system. With growing concerns about economic competitiveness and revenue stability, Landry’s initiative seeks to simplify the complex web of taxes and exemptions that currently burden residents and businesses alike. As lawmakers prepare to gather, Louisiana residents can expect a comprehensive discussion on potential reforms that could significantly impact their tax obligations and the state’s overall economic health.

“This special session fulfills the promise we made to the people of Louisiana to rebuild our economy and make Louisiana a place where people want to raise a family and create jobs,” said Landry last week. “Throughout this special session, we have the opportunity to give teachers a permanent pay raise, put more money in every worker’s pocket, eliminate the tax on prescription drugs, and provide much needed tax relief for seniors. I am eager to enact this new playbook and finally make Louisiana a beacon of hope—inviting families and businesses back home. It’s time we move Louisiana Forward.”

Landry is calling for a comprehensive examination of several aspects of Louisiana’s tax system as part of his proposed overhaul. Some key areas of focus include:

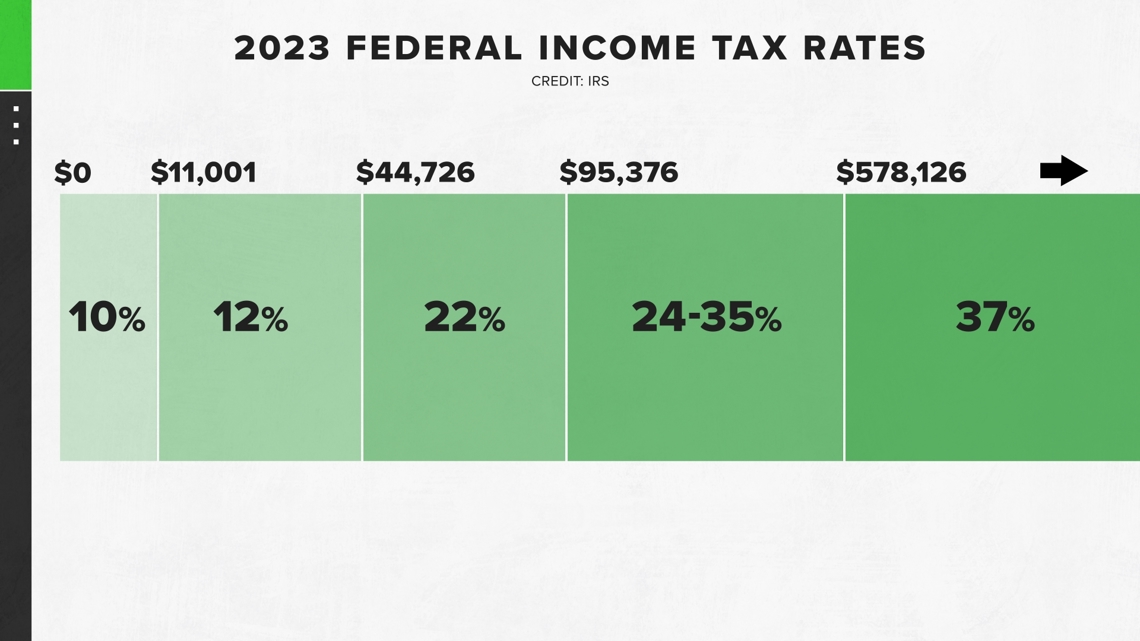

Individual Income Tax: The governor wants to explore legislation regarding income tax on estates and trusts, including aspects like rates, exemptions, deductions, reductions, credits and incentives. Additionally, there is a proposal to increase the standard deduction for individuals aged 65 and older.

Sales and Use Tax: Landry aims to legislate on both state and local sales and use taxes, addressing rates, exemptions, deductions, reductions, exclusions, credits, rebates and alternative reporting methods.

General Tax Legislation: Landry is interested in broader legislation regarding dedications, collections, revenues and taxes, alongside incentives aimed at economic development.

Digital Taxation: He intends to address the taxation of digital products, digital goods, digital services, and non-digital services.

Government Efficiency: There is a call for legislation concerning expenditure limits and identifying efficiencies and cost savings within state government.

Insurance Funding: Landry wants to legislate regarding the Louisiana Citizens Property Insurance Corporation to provide funding for fortified roof programs for policyholders.

Oilfield Site Restoration Fund: Proposed revisions for fees and administration related to the Oilfield Site Restoration Fund will also be examined.

Vocational Education Funding: Lastly, legislation to secure funding for purchasing instructional materials and supplies for students enrolled in vocational agriculture, agribusiness, or agriscience courses will be considered.

As Landry and lawmakers prepare for this critical session, the proposed reforms could have far-reaching implications for Louisiana’s tax structure and economic future. Residents are encouraged to stay informed and engaged as discussions unfold, as the outcomes may reshape how taxes impact their daily lives and the state’s economic landscape. For those seeking a deeper understanding, a primer on Louisiana’s tax structure (released in July 2024) is available here, providing insights into the key components of the state’s tax system.